The New Rules

The money is changing.

And so must we.

We all feel it.

The headlines about debt ceilings and deficits ... grocery bills that keep climbing. The uneasy sense that no matter how hard you work or how carefully you save, the ground beneath you is shifting, and unfortunately ...

You're not imagining it.

And what you do about it in the next few years will matter more than the last twenty. This report is a 20-minute read, and the people who understand what's in it will be positioned for what's coming.

The underlying reason is simple enough to understand, but it's bitter medicine. Most people would rather not think about it, and financial advisors would rather not explain it. Even scarier, politicians would definitely rather not reckon with it and just keep kicking the can down the road.

This report breaks it down as simply as possible — only the high-level details that matter for you as someone with a life to lead, a family to provide for, and a future to protect. I try to give just enough context to understand the truth of what's happening.

And at the end ... some actionable hope. Because while we can't control the forces swirling around us, we can take control of our own situation. That's what this report is for — to put you in the driver's seat of your own financial destiny.

Take a look at the Section Titles above to see where this report will take you.

Let's get into it.

Preface.

You feel it.

The headlines about debt ceilings and deficits. The grocery bill that keeps climbing. The sense that no matter how hard you work or how carefully you save, the ground beneath you is shifting.

You're not imagining it.

And what you do about it in the next few years will matter more than the last twenty. This report is a 20-minute read. The people who understand what's in it will be positioned for what's coming. The people who don't will wonder what happened.

The underlying reason is simple enough to understand, but it's bitter medicine. Most people would rather not think about it. Financial advisors would rather not explain it. Politicians would definitely rather not talk about it.

This report breaks it down as simply as possible — only the high-level details that matter for you as someone with a life to lead, a family to provide for, and a future to protect. No jargon. No fearmongering. Just the truth about what's happening and why.

And at the end ... some actionable hope. Because while we can't control the forces swirling around us, we can take control of our own situation. That's what this report is for — to put you in the driver's seat of your own financial destiny.

Take a look at the Section Titles above to see where this report will take you.

Let's get into it.

01

Our Elders'

Old Playbooks

Our great grandparents had a playbook.

Save in real money, buy land, hold gold and silver ... things you could touch and had been valuable for thousands of years.

Then in 1933, the government changed the rules. Roosevelt's Executive Order 6102 made it illegal for private citizens to own gold, and they were forced to turn it in at $20.67 an ounce. A year later, the government revalued gold at $35! If you'd followed the law and surrendered your gold, the dollars you received in exchange 'lost' 41% of its value overnight. I say 'lost' with incredulity because the reality is that the value was actively stolen. More on that in the next section. In short ... the responsible savers who played by the rules got punished for it.

Our great grandparents' playbook worked...

until the government made it illegal.

So our grandparents adapted ...

Find a good company; work there for forty years; retire with a pension that would pay you for the rest of your life. In short, in those days loyalty was rewarded and security was guaranteed.

Then in 1971, President Nixon severed the dollar from gold entirely. Overnight, the currency became unpredictable. Inflation surged, and suddenly, corporations couldn't project what their pension obligations would actually cost decades into the future. A promise to pay someone $2,000 a month in 1975 meant something very different by 2005. The pension didn't die because of greed or mismanagement — it died because fiat money made long-term promises impossible to keep. Promises made to workers over decades were broken in boardrooms and bankruptcy courts. The backbone of middle-class retirement was gone.

Our grandparents' playbook worked...

until the government altered the money.

So our parents adapted ...

Open a 401(k); contribute enough to get the employer match; buy mutual funds and trust the market to grow over time.

And it worked ... for a while. The assumptions seemed reasonable: steady growth, manageable inflation, tax rates in retirement that would be lower than during your working years. But those assumptions depended on a currency that behaved predictably — and a government that exercised restraint.

By the time you finish this report, you'll see how badly both of those assumptions have aged.

Our parents' playbook worked...

until the government money printer spun out.

Now it's our turn.

After three generations ...

After three failed playbooks ...

Three times the rules changed — not by market forces, but by policy decisions made in Washington — and the people who were caught unawares got fleeced.

Every. Time.

The rules are changing again, and most people don't see it yet. Their financial advisors — trained in the old system, compensated by the old system — aren't telling them. Because honestly, like every shift before, it takes time for the conversation to spin up and go mainstream ...

... but by the time everyone catches on it's almost too late.

Keep Reading.

By the end of this report, you'll come to understand:

What's happening to the money.

Why the old strategies won't work.

What the new rules look like.

02

What IS

Inflation?

I'll be blunt.

Your long-term savings success or failure hinges on your understanding of inflation.

The nature of inflation is often conflated with corporate greed. That's a deception, and it's time to learn & adapt. Because the truth is ... the game is almost up, and the world is about to cross the Rubicon whether you're prepared or not.

The good news is that the solution to being prepared is a simple enough formula, but what good is a solution if the problem isn't entirely understood?

PRICE INFLATION.

Here's the short of it:

Egg prices rising due to a mass culling of the egg-laying hen population causes a temporary shortage of egg supply ... prices rise because there's not enough eggs to go around and people still want the same amount of eggs.

That's PRICE INFLATION, and it's the one that slick politicians and media pundits like to point to because oh do we all love to have a boogeyman to blame. But when the egg supply catches back up, prices return to normal. So what's the deal with prices that rise and STAY there?

MONETARY INFLATION.

This is the nasty, more permanent form of inflation called MONETARY INFLATION, and no politician or allied media pundit likes to talk about it because there's only one entity to blame for this one ... government. And where price inflation is the result of not enough eggs to go around, monetary inflation is the result of TOO MUCH CURRENCY going around.

Too much currency?! How can there be such a thing??

Here's a handy thought experiment to understand it (it's much simpler than you think) ...

Let's give everyone LOADS of gold!

Everyone understands gold is valuable. But why?

The simple answer? Scarcity.

There's only so much of it and you can't print it or fake it. You can't make it (people have tried). Its rarity relative to everything else in the economy is what gives it worth.

Now imagine a meteor shower — gold raining down across every continent, piling up in backyards, clogging storm drains, filling swimming pools. Within weeks, gold would become just as common as driveway gravel... and just as worthless.

The properties of gold wouldn't have changed, but the supply would have, and now everyone would have it. Continue the thought experiment and let gold rain from the sky every year until it was more abundant than water ... you can imagine how quickly it would fall out of favor as a reliable store of value or medium of exchange.

Dollars work the same way.

When governments print currency faster than the economy grows, each dollar becomes less rare, less scarce, less valuable. The number in your bank account stays the same, but what it can actually buy shrinks.

We say its "purchasing power" has been lost.

While a gold meteor shower would be a random event, inflation and the loss of your purchasing power is anything but. Government policy around money printing is the sole culprit.

The Hidden Tax.

Here's what public schools rarely teach us:

Inflation hasn't always been the way of the world.

For most of human history, prices were relatively stable over long periods. A loaf of bread might cost roughly the same amount of silver for generations. In fact, a fine men's suit has cost roughly one ounce of gold for the last century or so (and still does!). You might say that the prices of bread and suits relative to gold have remained stable for generations.

The idea that everything should cost more next year than it did this year — that's a modern invention, and an entire school of economic theory has developed over the past century attempting to justify it.

Let's call it what it is: inflation is a hidden tax.

Think about it: if the government announced tomorrow that they were raising your taxes by 7% to directly fund their next war, there'd be outrage!

But when they simply print the money instead?

No vote required.

No angry constituents.

No political consequences.

The spending still happens, and the dollars still get created. But instead of taking money directly from your paycheck, they dilute the value of every dollar you've already saved by siphoning purchasing power from your bank account, your retirement fund, your children's college savings — silently, invisibly, year after year.

The entire world saving in dollars pays the tax. We just never see the bill.

When the government creates new dollars to fund its obligations, those dollars don't come from nowhere. They come from everywhere — from every existing dollar already in circulation. The pie doesn't get bigger, it just gets sliced thinner, making everyone's dollar savings worth less.

And unlike regular taxes, there's no deduction, no exemption, no accountant who can help you minimize the damage. The inflation tax hits everyone who holds dollars. The more you've saved, the more you lose.

The people who understand this don't keep their wealth in cash.

We're In the End Game.

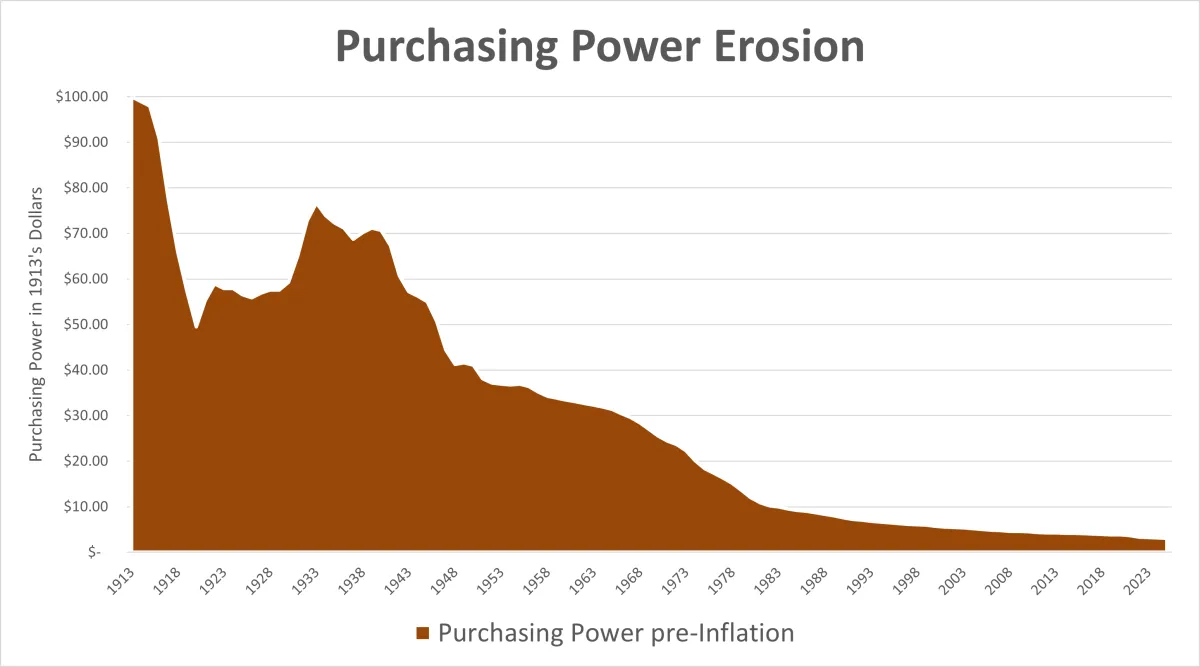

If you had spent a $100 bill in 1913, you could have ...

Covered three months of rent, and

Tailored a new suit or dress, and

Picked up a new pair of shoes, and

Bought 50 pounds of beef, and

100 loaves of bread, and

50 gallons of milk, and

20 dozen eggs, and

10 pounds of coffee, and

A dinner date out ...

... and likely STILL had change in your pocket!

Today, that same $100 might cover your groceries for a week or a couple tanks of gas. $100 saved in 1913 would purchase around $3 worth of 1913's goods or services today in 2026.

Have things gotten more expensive?

It sure feels that way ... but with technology and mass production, prices should be going DOWN as industry produces more with less inputs and greater efficiency.

The reality is ... the dollar has gotten WEAKER.

And its strength is almost entirely gone.

This is the end game.

Click to expand.

Tap to expand.

03

The 97%

Collapse

This mess has a beginning.

In 1913, Congress created the Federal Reserve - a private institution with private shareholders - and gave it control over the nation's money supply. What exactly does that mean? Everything else in the economy is, by and large, priced according to the ebbs and flows of supply & demand shifts. In other words, no central institution sets prices - the market and all its participants figure that out through a perpetual process called 'price discovery'.

Money is no different. With hard money like gold, the cost of money is discovered naturally — through the labor of mining it, refining it, transporting it, storing it, and lending it. With soft money like the US Dollar, that cost is simply decided. The Federal Reserve sets interest rates, and in doing so, sets the price of money by decree rather than by discovery. Imagine that - at the heart of the US economy is a market where NO ONE is allowed to participate in price discovery. A private institution decides (with heavy government pressure) what the price of money - the central economic lubricant - should be. And lucky us ... we get to see how the end of this century-long experiment will play out.

In 1913, a single dollar could buy what takes $31.36 to buy today!

Let that satisfyingly specific number sink in. One dollar in 1913 had the purchasing power of over thirty-one dollars today. Flip it around and today's dollar is worth about three cents in 1913 terms. Here's the hard truth:

The dollar has lost 97% of its purchasing power in just over a century.

This didn't happen by accident or by any 'natural' economic process. This wasn't any monetary voodoo magic too complex for "us normies" to understand. It has all been the result of government policy.

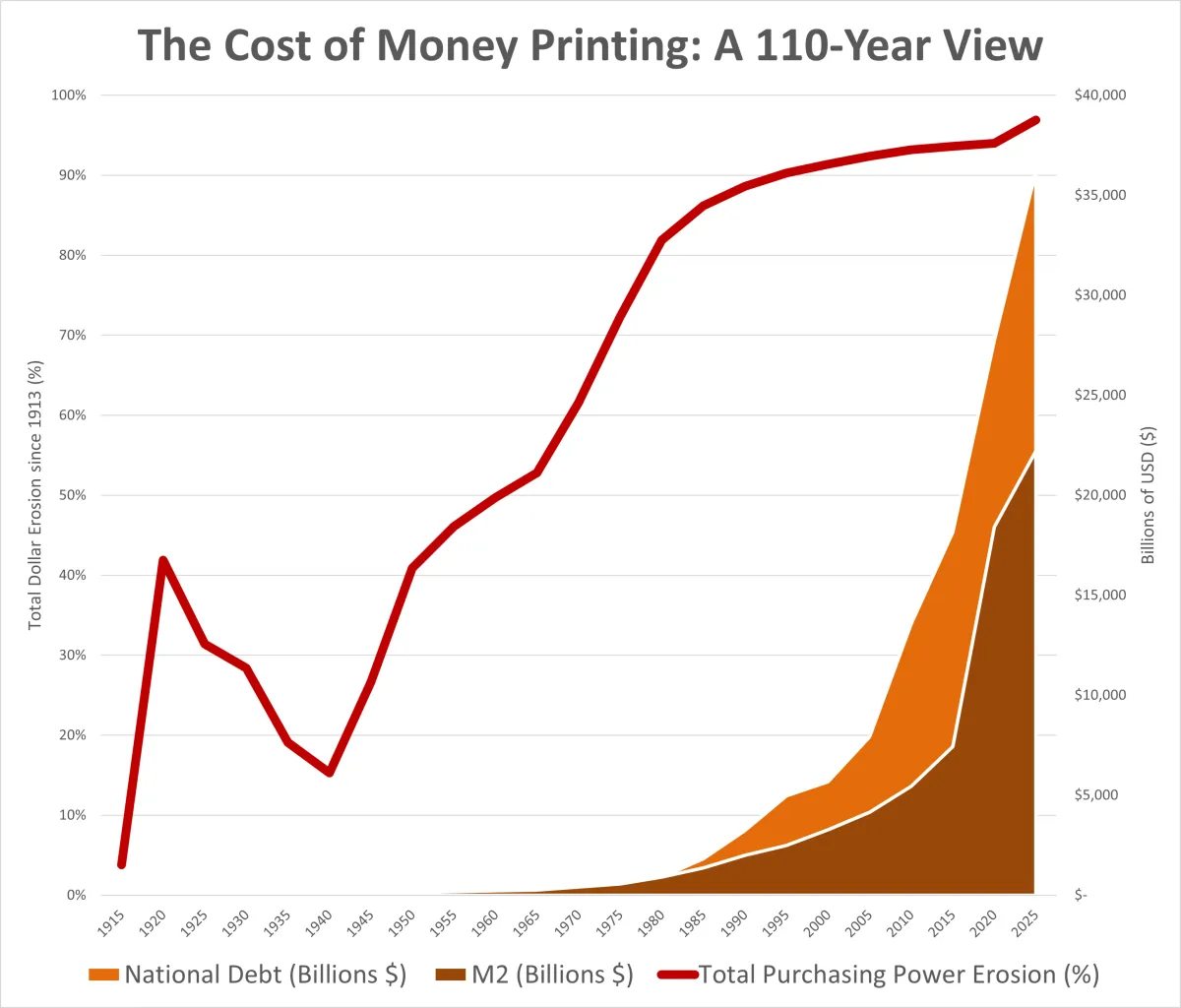

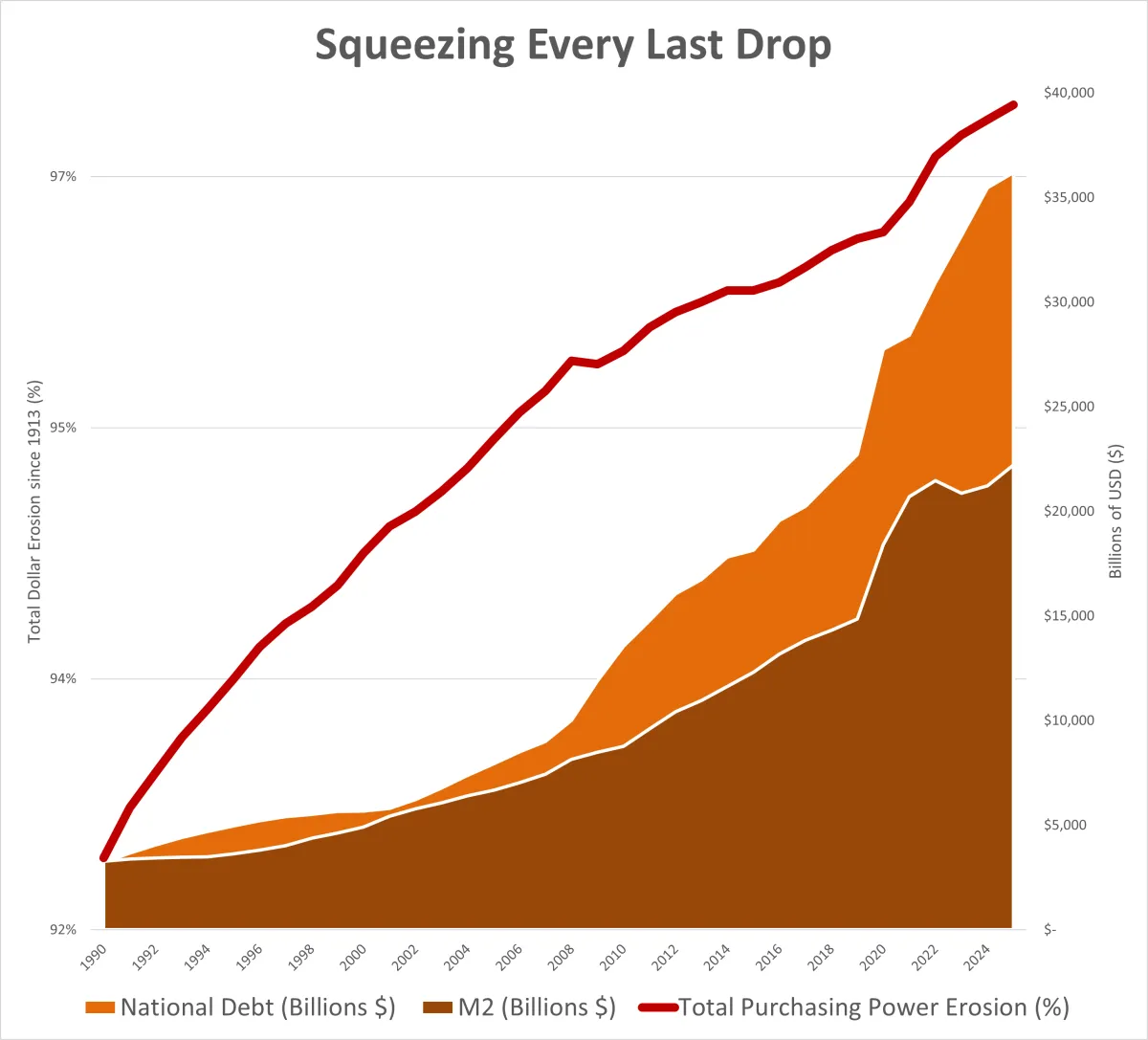

The chart below tells the story. The red line tracks cumulative purchasing power erosion (how much has been lost).

Click to expand.

Tap to expand.

Notice the spike to 42% by 1920 — that's World War I financing.

Then something unusual: the line drops through the 1930s, bottoming around 15% by 1940. That's deflation.

The Great Depression was brutal, but falling prices and a stagnating economy temporarily restored some of the dollar's value. After that? The line never looks back. It climbs through the postwar era, steepens after Nixon severed the dollar from gold in 1971, and pushes toward 90% by the turn of the millennium.

Now look at the brown and orange areas — M2 money supply and national debt respectively. M2 is the Federal Reserve's measure of "all the money" — every dollar in circulation, every checking account, every savings account, every money market fund. It's the total pool of liquid dollars sloshing around the economy. National debt is what the government owes.

These two metrics barely register for the first 70 years because the scale of what came later makes them invisible. The explosion begins after 2008. The vertical wall after 2020 represents more monetary expansion than the previous century combined.

And the red line? It flattens near 97% — not because erosion has stopped, but because there's almost nothing left to lose.

If you think that this game can continue on indefinitely because that's the way it's always been ... don't make the same mistake our elders made when the monetary order got rug-pulled out from under their feet!

A note before we continue

The next few sections walk through over a century of policy decisions — wars, social programs, bailouts, stimulus packages. Some were enacted by Republicans. Some by Democrats. Some had noble intentions. Some were naked political expedience.

This report takes no position on whether any of them were "worth it" or "wrong" or "right".

Money has a 'physics' to it — rules of cause and effect as reliable as gravity. Print more of it, and each unit becomes worth less. Arithmetic doesn't care who signs the bill. The same inflationary math that applies to a war applies to a social program or to a tax cut or a bailout or a foreign aid package. Intentions don't factor into the equation, only the numbers do.

What follows is an attempt to look at all of it with the neutrality of someone who says "for every action, there is an equal and opposite reaction" — not to score political points, but to understand what actually happened to your purchasing power and why.

In short, currency debasement through modern money-printing has consequences ... despite any and all "best intentions".

04

The Slow Bleed

(History)

1913 - 1971

The first era of dollar erosion began gradually.

World War I required financing.

The government issued bonds, and printed money to buy the ones the public wouldn't. Prices rose because the dollar weakened. But the war eventually ended, and things stabilized ... for a short while.

Then came the Great Depression, and in 1933 President Roosevelt changed the rules entirely.

Executive Order 6102 made it illegal for private citizens to own gold. Americans were forced to surrender their coins and bullion at $20.67 an ounce. A year later, the government revalued gold at $35.

Anyone who followed the law and turned in their gold in exchange for dollars saw those dollars lose 41% of their purchasing power overnight. Not through market forces but through executive decree.

This single act was the largest deliberate devaluation of the dollar in American history. The hidden tax, paid in one brutal stroke.

World War II brought another surge of money creation — though this time, gold flowed into American vaults as Europe paid for weapons and supplies. The U.S. emerged as the world's dominant economic power, and at Bretton Woods in 1944, the dollar became the global reserve currency. Other nations would hold dollars instead of gold, trusting that America would not print more dollars than it had gold in its vaults.

For a generation, it worked.

But do you think our policy leaders kept their end of the bargain?

Did the country's fiduciaries resist the urge to ... as the kids say these days ... make the 'money printer go brrr'?

Of course they didn't!

Cheap money (a.k.a. 'debt') flooded into the economy with plenty of countries and institutions to buy up the Treasury Bonds (government 'IOUs'). This era drove the expansion of America's legendary middle class and the innovation and industry that came with it ... and government spending never slowed down.

The Korean War. Vietnam. The Great Society programs — Medicare, Medicaid, and the expansion of the social safety net. Each initiative required funding. Each funding gap was filled with newly printed dollars. The only question we're asking here: where did the money come from?

By 1971, foreign governments had noticed and were fed up. France, in particular, parked a warship off the coast of New York City and demanded gold back in exchange for their dollar holdings.

They were calling America's bluff, and the rest of Europe soon followed suit.

By the time President Nixon faced this reckoning, the dollar had already lost roughly 60% of its 1913 purchasing power. Sixty years of wars, politically-rewarding pet programs, and myriad government promises — paid for with the silent erosion of every saver's wealth.

But what came next would make the first sixty years look like a warm-up.

05

The Age

of Fiat

(History)

1971 - 1990

On August 15, 1971, President Nixon went on television and changed the global monetary order.

He announced that the United States would temporarily 'shut the gold window' where none of the Bretton Woods stakeholders could redeem their paper dollars for real gold money.

The "temporary" suspension would become permanent. The last tether connecting American currency — and the rest of the currencies around the world — to anything tangible was severed.

Before 1971, the dollar's value was anchored — imperfectly, and often dishonestly, but anchored — to gold reserves. After 1971, the dollar's value became whatever the government said it was. The word for this is fiat — Latin for "let it be done" or simply "by decree."

The U.S. dollar was now pure fiat currency. Its value backed by nothing but faith and trust in the institutions that issued it.

But what happens when trust is broken and faith erodes?

Tap to expand.

Click to expand.

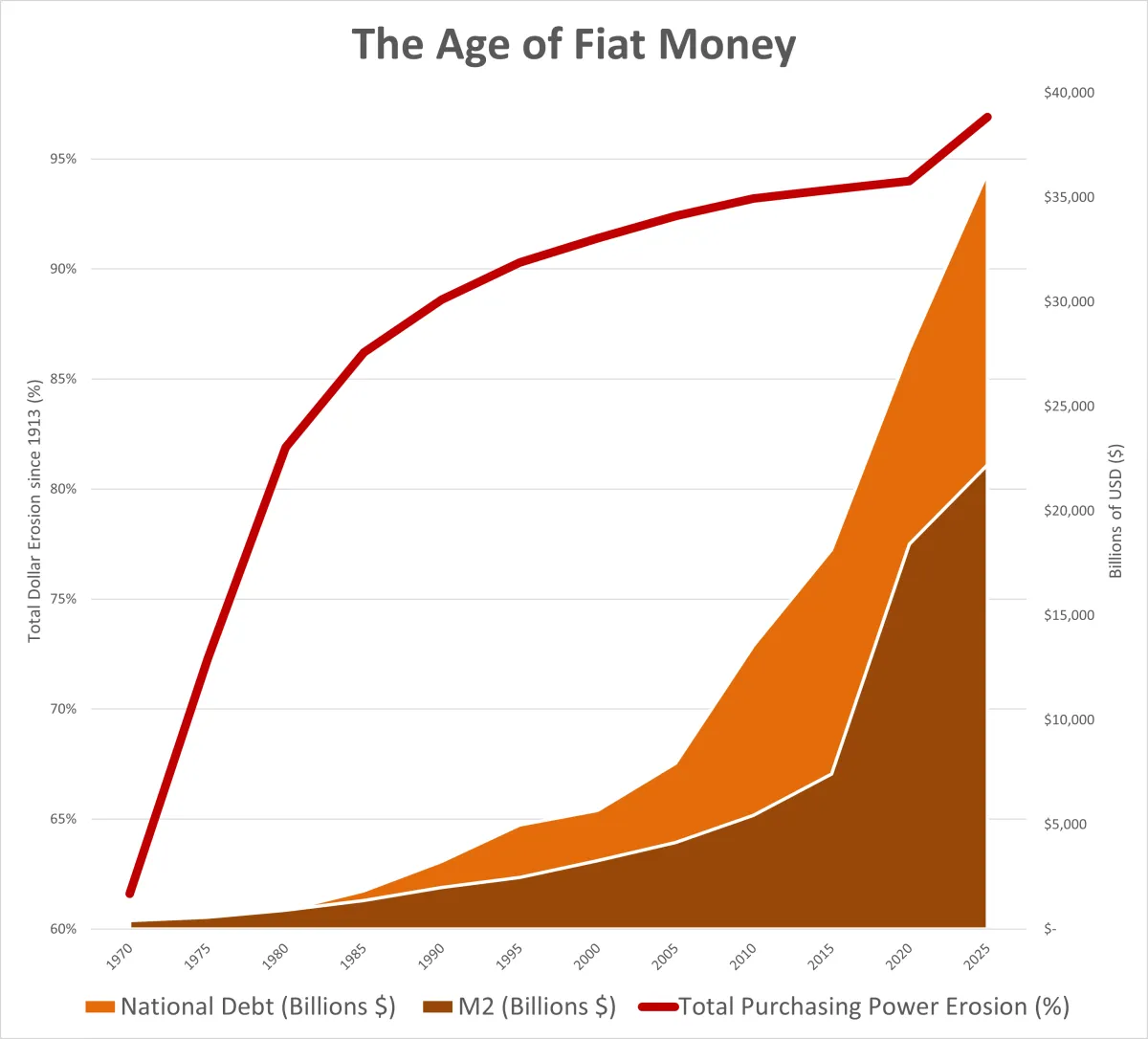

The consequences arrived quickly: look at the red line starting in 1970 — already at 61% total dollar erosion when Nixon made his announcement. See how steeply it climbed?

The 1970s brought oil shocks and 'stagflation' — the supposedly impossible combination of rising prices and economic stagnation. The government responded with more spending, more programs, more money creation. Social Security expanded. Energy subsidies proliferated. Each government "solution" required more dollars that didn't exist until they were conjured into being. By 1980, the red line had crossed 82%.

The 1980s brought new crises and a new innovation that would further debase our currency: bailout policies.

Black Monday in 1987 saw the stock market plunge 22% in a single day. The Federal Reserve flooded the system with liquidity to prevent collapse. The Savings and Loan crisis of the late 1980s — born of deregulation, speculation, and fraud — ended with taxpayers absorbing over $130 billion in losses.

The message was clear: when major financial institutions made catastrophic bets that failed, the government would print the money to make them whole ... the taxpayer would absorb the loss.

If those bets had won, do you think the taxpayer would have shared in the spoils?

Say it with me now ... "OF COURSE NOT!"

Critics call this 'privatized gains, and socialized losses'.

The party in power changes, but the pattern of money printing remains the same.

By 1990, the dollar had lost approximately 92% of its 1913 purchasing power. What had taken nearly six decades to erode by 60% took less than two more decades to erode by another 32%.

Now look at the brown and orange areas of that chart — M2 and national debt. In 1970, they're barely visible. By 1990, you can see them starting to grow. But look at the right side of the chart. You see that near-vertical wall after 2008? That's where we're headed next.

And here's where the math gets truly perverse.

06

Every Last Drop

(History)

1990 - Today

When you've already lost 92% of something, losing the remaining 8% might sound almost trivial. That last 8% is the graveyard where currencies go to die.

If there's one certainty in economics, it's this: all fiat currencies eventually collapse.

A comprehensive study of 775 fiat currencies throughout recorded history found that every single one followed the same trajectory — debased, inflated, and eventually collapsed or replaced. Not most, or the poorly managed ones. All of them. Every. Single. One.

The average lifespan is about 35 years, but of course there are exceptions. The British Pound is the oldest, but it has lost over 99% of its purchasing power since leaving the gold standard. The dollar has lost 97% since 1913. The disease is the same, and the only variable is how long the patient takes to die. And every time it happens, the ending plays out the same way: those who see it coming and reposition their wealth early tend to survive intact. Those who trust the system, who wait for officials to sound the alarm, who assume this time is different — they're the ones left holding worthless paper while their purchasing power is transferred to those who moved first.

Tap to expand.

Click to expand.

Look at this chart carefully. Notice how the national debt and money supply — the orange and brown areas respectively — explode upward while the red line of purchasing power erosion barely moves? That's the brutal mathematics of the end stage at work.

To extract the first 60% of the dollar's purchasing power, the government needed to print a few hundred billion over six decades.

To extract the next 32%, they printed trillions over two decades.

To squeeze out the last 8%? They've printed tens of trillions in just the past few years alone.

This is the nature of exponential decay. Each remaining percentage point of purchasing power requires more money printing than all the previous points combined. And every dollar of debt created requires future dollars to service it — dollars that must also be printed, further diluting what remains.

The hits kept coming ... the Gulf War, the dot-com crash, 9/11 retribution, foreign aid packages, and the sprawling War on Terror ...

Acronym-agencies with thousands upon thousands of grant projects injecting dollars all around the world.

Each crisis or policy decision was met with the same solution: print more, spend more, figure it out later.

Then came 2008.

The housing bubble — inflated by easy money and enabled by institutions that knew they'd be bailed out — finally burst. The response dwarfed anything that came before.

Bank bailouts, quantitative easing, trillions created from nothing to prevent the financial system from seizing up entirely.

The Affordable Care Act added new long-term obligations. Entitlement spending programs continued their upward march. The national debt, already staggering, began its vertical climb.

And then came 2020.

The pandemic response made 2008 look modest: direct payments to citizens; payroll protection; stimulus upon stimulus ...

Approximately 40%of all U.S. dollars in circulation were conjured into existence in roughly the last four years.

The result? The inflation surge of 2021–2024 was a mathematical certainty. And despite what you've heard about inflation "cooling," prices haven't returned to pre-pandemic levels.

Don't expect them to. They won't. The dollars measuring prices across the economy have been permanently diluted. Inflation 'cooling' just means government isn't debasing the currency as fast ... not that they've stopped.

Here's the number that should keep our leaders up at night: the national debt now exceeds the entire M2 money supply. The government owes more than all the currency currently in circulation — printed, minted, or existing on a digital ledger. The only way to service that debt is to create more dollars. And creating more dollars extracts what little purchasing power remains.

This is the negative feedback loop that kills currencies. And it's accelerating.

07

Why This Won't Stop

Let's bring this all to a head.

The U.S. national debt has surpassed $36 trillion. Interest payments on that debt now exceed $1 trillion per year — larger than the entire defense budget. The only way to service that debt without defaulting is to continue issuing new debt. And the only way to issue new debt is to make it attractive enough for buyers to want it.

That used to be easy. Foreign governments — China, Japan, Saudi Arabia — lined up to buy U.S. Treasuries because they were the safest bet on the planet. But the buyer pool is shifting. The largest economies — the U.S., China, Japan, the EU — are all running massive deficits and printing money to cover them. The nations with healthy balance sheets, like Saudi Arabia, have their own priorities now. And everyone is watching America's fiscal trajectory with growing skepticism.

So what makes U.S. debt attractive when buyers have options? Higher interest rates — better returns for lenders.

But there's a catch. And it's a doozy of a paradox.

Fiscal Dominance.

Economists call it "fiscal dominance" — a condition where government debt grows so large that it begins dictating monetary policy instead of the Fed doing so. The Federal Reserve faces two paths, and neither leads anywhere good.

Path #1 ➜ Raise Rates, Help Investors, Print Slower, Less Spending

Higher yields make U.S. debt more appealing. Buyers line up again. In theory, this also slows government spending because borrowing becomes expensive — fiscal discipline enforced by market pressure. We all understand balanced budgets. When the kids overspend on the credit card, you cut them off.

But we're not starting from zero. We're starting from $36 trillion in existing debt — debt that constantly matures and needs to be refinanced. As old bonds come due and get rolled into new ones at higher rates, the average interest cost climbs. We're already paying over $1 trillion a year. As more of that debt rolls over at higher rates, the number keeps growing — a slow-motion squeeze that eventually becomes unsurvivable. The government would have to borrow even more just to cover the interest. A death spiral that ends in default. The bubble that's been inflating for decades pops all at once.

Path #2 ➜ Lower Rates, Hurt Investors, Print Faster, Keep Spending

Low rates make borrowing cheap. Government spending flows freely. But buyers lose interest — why lend to an indebted government for a 2% return when inflation is eating 3%? For decades, buyers accepted low yields because U.S. Treasuries were the safest asset on Earth. "The full faith and credit of the United States" meant something. That trust has been shaken.

So what happens when rates are too low to attract buyers? The Federal Reserve steps in as the buyer of last resort. It creates dollars and uses them to purchase Treasury debt. The government issues the bonds; an institution it created buys them with money it conjured from nothing. Economists call this "debt monetization." It's not quite lending to yourself — but it's close enough that the distinction stops mattering.

The dollar continues to debase. Your purchasing power erodes. But the system stays intact — hopefully — long enough to manage the decline.

Path One is a heart attack.

Path Two is a slow poisoning.

The destination is the same.

Only the timeline differs.

The Fed has chosen Path Two. Not because it's good policy, but because a slow bleed is preferable to sudden cardiac arrest. Decades of monetary experimentation have painted them into a corner where the only option is to keep walking deeper — and hope they find a door on the other side.

And here's the uncomfortable truth about how we got here: fiscal responsibility doesn't win elections. The age of balanced budgets and shrinking the debt — if it ever really existed — is long gone. Our country's leadership figured out decades ago that promising new spending programs is how you collect votes. Austerity doesn't have a constituency. Cutting programs loses donors. The political incentives all point in one direction: spend more, print more, worry about it later.

Every major spending proposal — whether it comes from the left or the right — requires either higher taxes, deeper debt, or more money printing. State and local governments face similar pressures. Pension obligations they can't meet. Infrastructure gaps they can't fund. Unfunded liabilities that compound year after year.

None of this is partisan. Both parties got us here, and neither has a plan to get us out.

THE END GAME SPIRAL

01.

PROBLEM: Competing Obligations

Government has stacked up competing obligations - voters and donors want programs, bond holders want their gold.

SOLUTION: Sever the Gold Standard

Sever the gold connection and go to a fiat standard. Now government can print currency to satisfy BOTH obligations without choosing.

02.

PROBLEM: Politics Exceeds Revenues

Unconstrained, politicians keep accruing donor and electorate obligations AND selling IOUs to bond holders to pay for them. Pretty soon, obligations exceed tax revenues.

SOLUTION: Deficit Spending

Deficit spend. Borrow from the future to pay for now.

03.

PROBLEM: Deficits & Debts Exceed GDP

Debt grows so large it surpasses the entire GDP. Interest payments alone hit billions and then trillions per yer.

SOLUTION: Refinance Old Debts into New Debt

Borrow even more to pay for obligations AND debt service. Roll old bonds into new bonds. Keep the game going.

04.

PROBLEM: Buyer Confidence in the U.S. Wanes

Confidence in the full faith and credit of the United States begins to wane. Buyers start asking: "Can they actually pay this back?"

SOLUTION: Raise Interest Rates

Raise interest rates. Higher yields compensate buyers for the increased risk. Better returns attract buyers back to the auction.

05.

PROBLEM: Interest Payments Spiral and Balloon

Higher interest rates mean higher interest payments. The government is now borrowing just to cover the interest on previous borrowing. Debt service costs threaten to spiral out of control.

SOLUTION: Government Pressures for Lower Rates

Political pressure mounts to lower rates. The Executive Branch needs cheaper borrowing to keep the government solvent and fund its agenda.

06.

PROBLEM: Fiscal Dominance & Fed Resistance

The Federal Reserve is designed to be independent. Its mandate is price stability, not funding government deficits. The Fed Chair resists.

SOLUTION: Executive Branch Replaces Fed Leadership

Replace Fed leadership. Nominate a Chair aligned with the administration's priorities. Remove the obstacle.

07.

PROBLEM: Inflation Outpaces Treasury Yields

The new Fed lowers rates as intended. But lower yields mean bond buyers are now earning less than inflation. They're losing purchasing power by lending to America.

SOLUTION: Buyers Exit Treasuries

Foreign governments and institutions start exiting Treasuries. China reduces holdings from $1.3 trillion to under $800 billion. The money flows into gold, other currencies, anything that holds value better than a dollar-denominated IOU.

08.

PROBLEM: Treasury Buyers Dry Up

Fewer buyers at the auction. The pool of willing lenders is drying up. But the government still needs to fund its deficit.

SOLUTION: Fed Prints to Buy

The Federal Reserve steps in as buyer of last resort. It creates dollars out of nothing and uses them to buy the bonds no one else wants. The government issues debt; an institution it created purchases that debt with money it conjured.

09.

PROBLEM: Currency Debases Further

Every new dollar dilutes every existing dollar. More dollars chasing the same goods. Purchasing power erodes. Prices rise. The currency debases.

SOLUTION: Buyer Exit Accelerates

Remaining buyers accelerate their exit. More capital flees to gold, commodities, foreign currencies — anything that holds value better than a debasing dollar.

10.

PROBLEM: Even Fewer Treasury Buyers (lenders)

The buyer pool shrinks even further. But the government's obligations haven't shrunk. Deficits continue. Someone needs to buy the bonds.

SOLUTION: Fed Keeps Printing

The Fed prints even more. Steps in as an even larger buyer of last resort.

∞

PARADOX: The Self-Perpetuating Negative Feeback loop

Politicians won't stop spending - elections demand it. Deficits grow - Treasury issues more debt. Lender confidence erodes - buyers demand higher yields or won't lend. Fed prints to buy what markets won't. Printing debases the currency - inflation rises. Bond yields outpaced by inflation - fewer lenders show up to buy bonds.

It's An

Everything Bubble

The system is working exactly as designed.

Fiat currency — money backed by nothing but government promise — requires debt creation to function. Every dollar in circulation was borrowed into existence. Growth in a fiat system means growth in debt. The architecture demands it. Economists have a term for where this leads when carried to its logical conclusion: an "everything bubble." Asset prices inflate because the currency keeps losing value. Stocks go up. Real estate goes up. Everything goes up — measured in a unit that keeps shrinking. The bubble is in the money itself.

That's the poison pill baked into the foundation. And now the dosage is accelerating.

How long can this continue? Years? Decades?

Look at who's actually moving.

Giants

Are Moving

Warren Buffett sold over $134 billion in stocks in 2024 and built a cash reserve exceeding $380 billion. Berkshire has been a net seller for twelve consecutive quarters. When asked why: "Often, nothing looks compelling."

Michael Burry — the man who shorted the housing market before 2008 — deregistered his hedge fund and has been loading up on put options. Same pattern he ran before the last crisis.

China has slashed its Treasury holdings by 45% — from $1.3 trillion to under $760 billion — while accumulating gold at record pace. In June 2025, the Shanghai Gold Exchange opened offshore vaults in Hong Kong allowing foreign holders to convert yuan directly to physical gold. Cross-border yuan settlement has climbed to 32% of China's trade, up from 18% three years ago.

Foreign ownership of U.S. Treasuries has fallen from over 50% to roughly 30%. The dollar's share of global reserves has dropped from 72% in 2001 to 56% now — a 30-year low. That decline took two decades. The next leg down won't.

It's An

Everything Bubble

The system is working exactly as designed.

Fiat currency — money backed by nothing but government promise — requires debt creation to function. Every dollar in circulation was borrowed into existence. Growth in a fiat system means growth in debt. The architecture demands it. Economists have a term for where this leads when carried to its logical conclusion: an "everything bubble." Asset prices inflate because the currency keeps losing value. Stocks go up. Real estate goes up. Everything goes up — measured in a unit that keeps shrinking. The bubble is in the money itself.

That's the poison pill baked into the foundation. And now the dosage is accelerating.

How long can this continue? Years? Decades?

Look at who's actually moving.

Giants

Are Moving

Warren Buffett sold over $134 billion in stocks in 2024 and built a cash reserve exceeding $380 billion. Berkshire has been a net seller for twelve consecutive quarters. When asked why: "Often, nothing looks compelling."

Michael Burry — the man who shorted the housing market before 2008 — deregistered his hedge fund and has been loading up on put options. Same pattern he ran before the last crisis.

China has slashed its Treasury holdings by 45% — from $1.3 trillion to under $760 billion — while accumulating gold at record pace. In June 2025, the Shanghai Gold Exchange opened offshore vaults in Hong Kong allowing foreign holders to convert yuan directly to physical gold. Cross-border yuan settlement has climbed to 32% of China's trade, up from 18% three years ago.

Foreign ownership of U.S. Treasuries has fallen from over 50% to roughly 30%. The dollar's share of global reserves has dropped from 72% in 2001 to 56% now — a 30-year low. That decline took two decades. The next leg down won't.

These are positions, not predictions. The biggest players on Earth are repositioning their wealth into hard assets, reducing exposure to dollar-denominated paper, and building parallel financial infrastructure that doesn't require American permission to operate.

Debt-to-GDP has already crossed 121%. Economists have long warned that 90% is the danger zone — the point where debt begins to drag on growth. We blew past that marker years ago. We're deep into territory where the math becomes self-reinforcing: borrow to pay interest, print to cover what you can't borrow, watch the currency debase, repeat.

Cost of living keeps climbing. Groceries. Housing. Healthcare. Insurance. The official inflation numbers say it's moderating. Your bank account says otherwise. The gap between reported inflation and lived experience grows wider every month — and that gap is the slow leak most people don't notice until they're underwater.

The Math

Never Lies

This is now.

The institutions see it. The governments see it. The ultra-wealthy see it. They're moving — quietly, steadily — while the rest of the world debates whether anything is really wrong.

The people still following the old playbook — save in dollars, trust the system, wait for retirement — are standing on a floor that's dissolving beneath their feet. Nobody told them the rules changed.

Consider yourself informed :

THE RULES HAVE CHANGED.

The Rules Have Changed.

The Math

Never Lies

These are positions, not predictions. The biggest players on Earth are repositioning their wealth into hard assets, reducing exposure to dollar-denominated paper, and building parallel financial infrastructure that doesn't require American permission to operate.

Debt-to-GDP has already crossed 121%. Economists have long warned that 90% is the danger zone — the point where debt begins to drag on growth. We blew past that marker years ago. We're deep into territory where the math becomes self-reinforcing: borrow to pay interest, print to cover what you can't borrow, watch the currency debase, repeat.

Cost of living keeps climbing. Groceries. Housing. Healthcare. Insurance. The official inflation numbers say it's moderating. Your bank account says otherwise. The gap between reported inflation and lived experience grows wider every month — and that gap is the slow leak most people don't notice until they're underwater.

The Rules Have Changed.

This is now.

The institutions see it. The governments see it. The ultra-wealthy see it. They're moving — quietly, steadily — while the rest of the world debates whether anything is really wrong.

The people still following the old playbook — save in dollars, trust the system, wait for retirement — are standing on a floor that's dissolving beneath their feet. Nobody told them the rules changed.

Consider yourself informed :

THE RULES HAVE CHANGED.

08

Build

Your Ark

Now you understand the problem. Here's what to do.

Currency debasement is not new.

Governments overextend. Debt accumulates. The currency weakens. This pattern has repeated across centuries — Roman denarii, Weimar marks, Argentine pesos, and now the U.S. dollar. The timeline varies. The destination does not. The response from those who preserved wealth has been consistent:

They owned ASSETS that appreciate faster than the currency depreciates.

The ultra-wealthy don't think about 'saving money'. Rather, they store value.

Their portfolios emphasize equity in productive businesses, real estate, and structured financial instruments designed to capture growth while minimizing tax exposure. They access liquidity through loans against appreciating collateral rather than selling positions. They transfer wealth to heirs through vehicles that bypass estate taxation entirely. The family offices and private wealth managers serving the top 1% have built entire disciplines around these principles.

Meanwhile, the standard saver holds cash and cash equivalents.

Savings accounts. CDs. Money market funds. Stacks of paper cash. These feel safe because the number never goes down. But the purchasing power does — every year — and most people don't notice until decades of erosion have compounded into a retirement shortfall and suddenly things have gotten so expensive that there's loads more life at the end of the money.

So what does work?

Assets that appreciate faster than currency depreciates.

That's the formula. The wealthy have operated by it for generations. Real estate. Business equity. Structured financial instruments. Self-structured family pension strategies. The specific vehicles vary, but the principle holds: convert dollars into things that gain value while dollars lose it.

For most Americans, the question becomes practical: what assets are actually accessible without a family office, a seven-figure minimum, or a team of attorneys? The 401(k) and mutual fund have been the standard answer for decades, but they were built for a different era. Too many fees, too much risk exposure, and unfavorable tax treatments are not the tools for rising water levels and heavy rainfall.

The answer lies in a category of financial instruments that most people have never been introduced to because they aren't typically part of the corporate conversation.

These instruments share common characteristics:

Grows with the market

Protected from market crashes

Fees don't compound against you for decades

Tax-free growth — not tax-deferred, tax-free

Accessible without penalty before retirement age

Accessible without compounding interruptions

Transfers to heirs without triggering a tax event

Following certain provisions in the tax code will lead one to asset classes better suited for the changing monetary order. They've survived multiple administrations, tax overhauls, regulatory reviews, and they remain available to anyone who bothers to look.

So why aren't they part of the mainstream conversation?

The financial services industry is built around assets under management. Advisors are trained in securities. Compensation structures reward products that keep capital inside fee-generating accounts. And honestly? Tradition plays a big role.

The system trains advisors for one set of tools, compensates them for recommending those tools, and never introduces the alternatives. Most advisors recommend what they know. What they know was built for a different era.

09

The Three Leaks

Be warned ...

You can own assets and still lose.

You can hold a "sector diversified" portfolio and watch it evaporate in a market crash the year before you retire. You can invest for decades and surrender a third of your gains to fees so buried in fine print that you never see them until the papercuts have piled up. You can build a nest egg over a lifetime and hand a significant portion to the IRS the moment you access it.

These are the leaks. They drain wealth quietly, steadily, even when you're doing everything "right." They're baked into the instruments of the old playbook — remnants of an era when slow leaks didn't matter because the bucket was filling faster than it could drain.

The bucket is no longer filling faster because everything's more expensive.

Leaky assets are easy to identify once you know what the three main leaks look like.

RISK.

Market exposure can erase years of gains in weeks.

We've been conditioned to think of investing as picking winners — buy the right stock, hope it goes to the moon. That casino mentality has its place for speculative plays with money you can afford to lose.

But your foundation? The wealth you're counting on to fund your retirement, protect your family, sustain your lifestyle when the paychecks stop? That should not be a bet.

The market doesn't owe you a recovery. A crash in the wrong year can permanently alter your trajectory. You don't get those years back.

The patch:

Instruments with contractual downside protection.

Guaranteed floors written into the structure.

Appreciation that participates in market upside without exposure to market crashes.

FEES.

A 1% annual fee doesn't sound like much.

Over 30 years, it consumes nearly a third of your potential gains. The average 401(k) carries expense ratios, management fees, and administrative costs that compound silently against your balance every year. You never see a bill. You just retire with less than you would have.

The math is not controversial. It's just not advertised.

The patch:

Fee structures that don't compound annually against your balance.

Costs that shrink proportionally as your account grows, not expand.

Transparency on what you're paying and when.

TAXES.

Every dollar in a tax-deferred account is a dollar the government has a claim on.

The 401(k) and traditional IRA postpone taxation — they don't eliminate it. The rate you'll pay at withdrawal depends on future tax policy, your income in retirement, and how much you need to access in any given year. Pull out more, get bumped into a higher bracket. The government's share grows alongside yours.

And at death? The balance transfers to your heirs as taxable income.

The patch:

Vehicles that compound tax-free under current IRC provisions.

Access mechanisms that don't trigger taxable events.

Death benefits that transfer to heirs income-tax-free.

10

Onward.

Take this next step.

You cannot control the Federal Reserve. You cannot control Congress. You cannot control what China does with its gold reserves or how quickly the BRICS coalition builds its alternative systems.

But you can take control of your own situation. First, come to terms with this:

Currency crises are not new. Neither is what happens during them.

They've happened again and again throughout history, and the general effect is a recurring pattern:

Wealth transfers — massively — from those who don't see it coming to those who do. From those sitting in cash to those holding appreciating assets. From those following yesterday's playbook to those who adapted in time. This pattern has repeated across centuries, and it is already underway now. The smart money is moving quietly and steadily. The institutions know. The ultra-wealthy know. Foreign governments know.

Now you know.

Protection is Simple

Own assets that don't leak. Park as much value as you can into instruments that grow, that are protected from downside risk, and that don't drain silently to fees and taxes while the currency system consumes itself.

Simple in principle. Harder in practice.

The landscape of assets is broad, full of choices, and deliberately complex. If you're fortunate enough to be in a position to save — and if anything in this report has convinced you that the traditional route may not be the safest path forward — then the next question is obvious: where do you even start?

The answer is to step back before stepping forward. Assess where you currently stand before deciding where to go.

Protection is Simple

Own assets that don't leak. Park as much value as you can into instruments that grow, that are protected from downside risk, and that don't drain silently to fees and taxes while the currency system consumes itself.

Simple in principle. Harder in practice.

The landscape of assets is broad, full of choices, and deliberately complex. If you're fortunate enough to be in a position to save — and if anything in this report has convinced you that the traditional route may not be the safest path forward — then the next question is obvious: where do you even start?

The answer is to step back before stepping forward. Assess where you currently stand before deciding where to go.

The LeakScore Report

Start here.

Take a step back and assess your current situation using this free self-diagnostic tool I built: The LeakScore Report.

Twenty-three questions. About four minutes. No account numbers. No sensitive financial details. Just honest answers about how you think about money, how your current strategy is structured, and where your priorities are.

The report measures your exposure across the three dimensions covered in this report — risk, fees, and taxes — and delivers a personalized breakdown of where your leaks are.

Hi!

I'm Marina Moses.

I spent over 15 years in corporate finance helping publicly traded and Fortune 500 companies shape more than a quarter billion in outcomes.

Now I structure private wealth strategies for regular people like you so you can protect and grow your hard-earned capital -- using boardroom strategies & principles most financial advisors never talk about.

I developed the LeakScore Report because you deserve better than 'save more, diversify, and hope.' Inflation may slow down, but it will never reverse. Your savings need to be in assets. And those assets need to be protected from risk, fees, and taxes. The wealthiest families figured this out decades ago. It's time you saw it too.

Hi!

I'm Marina Moses.

I spent over 15 years in corporate finance helping publicly traded and Fortune 500 companies shape more than a quarter billion in outcomes.

Now I structure private wealth strategies for regular people like you so you can protect and grow your hard-earned capital -- using boardroom strategies & principles most financial advisors never talk about.

I developed the LeakScore Report because you deserve better than 'save more, diversify, and hope.' Inflation may slow down, but it will never reverse. Your savings need to be in assets. And those assets need to be protected from risk, fees, and taxes. The wealthiest families figured this out decades ago. It's time you saw it too.